Building Resilient Supply Chains for Any World Scenario

In today’s highly interconnected economy, supply chain resilience is no longer just a defensive strategy…

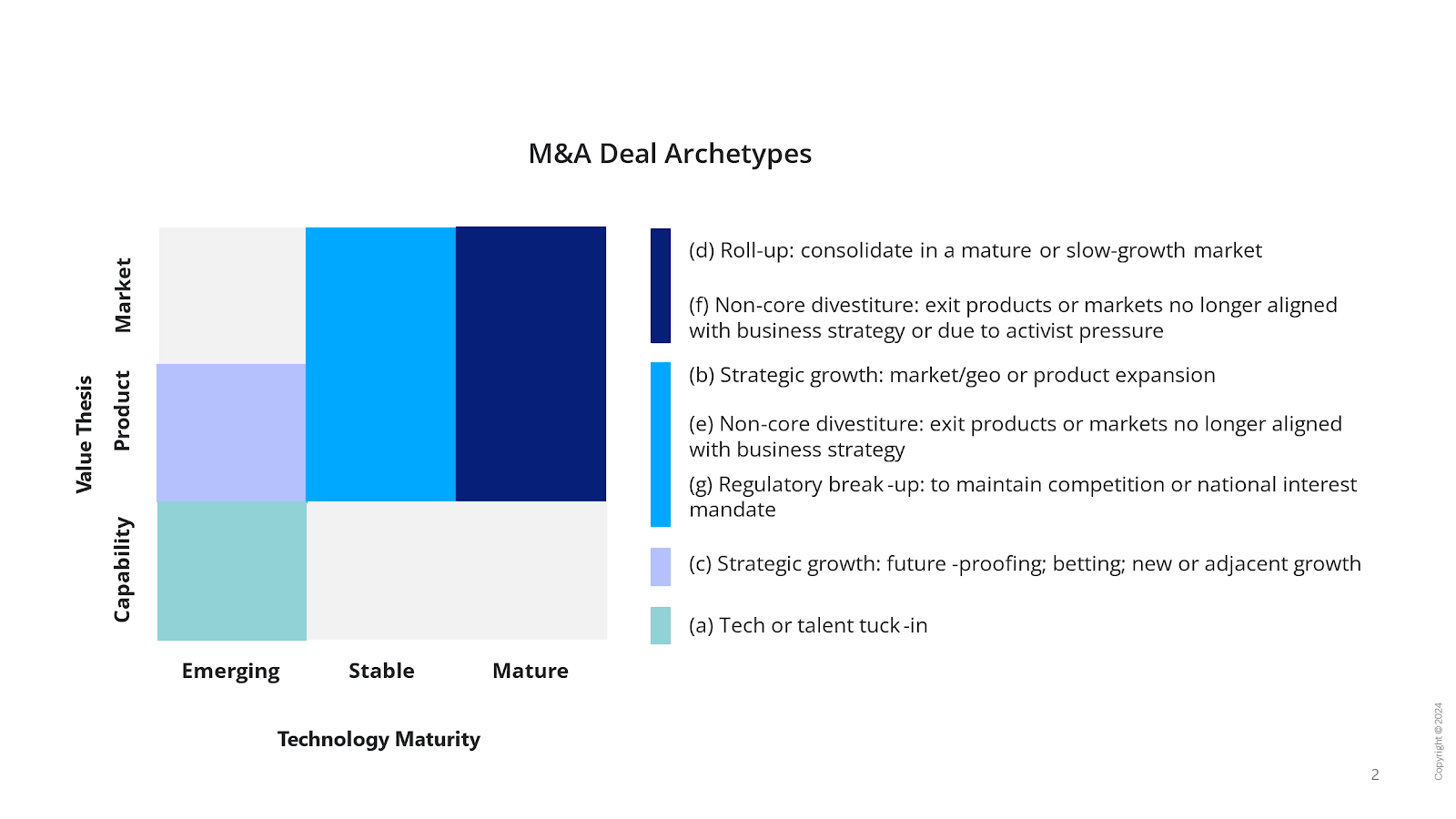

With the continued momentum of genAI, paired with a more friendly regulatory environment, M&A activity can experience tailwinds in 2025 and beyond. This presents opportunities for companies to be more aggressive but requires them to be thoughtful in their M&A moves—both during diligence and integration or carve-out. To help decision-makers prioritize their M&A strategies and tactics, we explore four drivers (market, product, capability, regulatory) that influence the archetype of technology (emerging, stable, or mature) deals.

The global tech M&A landscape has continuously evolved:

Understanding the drivers of the deal and the resulting archetypes enables organizations to identify the opportunities most aligned with their strategic objectives and be a “prepared buyer or seller” and eventually execute a successful deal.

Starting with the business strategy and specific objectives helps determine how best to take advantage of the drivers that impact the nature and success of an M&A deal. For instance, do you want to expand into a new market? Acquire new technology to leapfrog a competitor? Do you want to shed a declining business? Each of the strategies directs you to evaluate potential deal archetypes, e.g., a strategic market acquisition in a new country, a tech tuck-in, or a non-core divestiture.

Tech M&A strategies are influenced by four drivers, with seven archetypes, (a) through (g), below:

(a) Tech and Talent Tuck-ins: Acquisitions of niche technologies or teams to gain technical expertise or innovation (e.g., a mobile devices company acquiring hinge technology for foldable devices).

(b) Strategic Growth (Market/Geo, Business Model Evolution): Focused on expanding market reach or evolving business models, such as moving into subscription-based services (e.g., gaming company acquiring cloud gaming software to expand SaaS).

(c) Strategic Growth (Cross-Industry): Cross-industry technology acquisitions, such as healthcare firms acquiring telehealth platforms to enhance service offerings.

(d) Mature Consolidation: Consolidating underperforming or saturated markets (e.g., printer companies merging to streamline R&D and production operations).

(e) Non-Core Divestitures: Companies spinning off non-core assets, such as a legacy software product, to focus on cloud offerings.

(f) Activist Carve-Outs: Divisions spun off under investor pressure or as part of a strategic separation to unlock shareholder value (e.g., tech company separating a slow-growth business unit or to renew focus on each business unit).

(g) Regulatory Break-Ups: Mandated divestitures or concessions driven by regulatory pressures (e.g., platform companies exiting specific markets or products to comply with antitrust laws or foreign investment requirements).

While the four drivers offer strategic guidance to craft a deal and the seven archetypes offer a roadmap for tactical M&A execution, below are broad challenges to be prepared for:

To maximize value from tech M&A in 2025 and beyond, Tech companies must:

M&A is no longer a growth strategy just for medium to large companies. It’s a choice for companies of all sizes. Going into it with eyes wide open is necessary to improve the odds of success and being in the ~30% of companies that create value from M&A.CI

Copyright © 2024 CASETEAM - All Rights Reserved.

CASETEAM and the CASETEAM logo are Service Marks of`

CASETEAM LLC

Share this Post